Being long time travelers can be a wonderful thing, especially if we decide to travel with purpose. It can also be a lifestyle philosophy that can cost you less than the cost you are currently paying to stay at home. But when we shared with people that we traveled the world for less than $30K during our first year and that we only spent $8 to pay for healthcare insurance, they were wondering if this number was bogus or if we have decided to entirely opt out of healthcare insurance.

In this article, we will add some clarification and dig into the large topic of health care insurance. We will explain (1) how we got coverage in California in 2019 for $1 per person and per month, (2) what insurance we decided on for year 2, (3) why we think our health care costs are going to be a fraction of what they are in the US (even if we pay out of pocket) and (4) why we believe that we (and most people) will be saving thousands of dollars each year by avoiding the US healthcare system. Ready to talk about health care?

Year 1 of Nomadic Travel – The $8 insurance cost

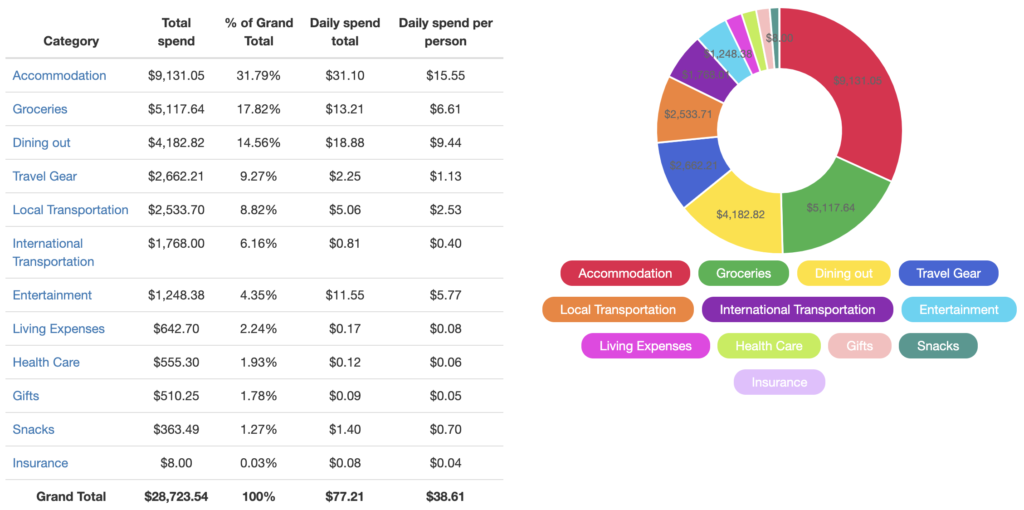

If you dig into our 1st Year of Nomadic Travel Spending Report you will see costs for both “Health Care” and “Insurance” (see graph above for summary view and tables below to get to the details).

Note: We categorize under “Health Care” any out of pocket expense related to our health (including Dental care) and we categorize under “Insurance” any insurance costs we incur.

During our 1st year of Nomadic Travel, our “Insurance” cost was $8 while our “Health Care” cost was $555.

During year 1, Mrs. NN was working remotely because her company allowed her to work from anywhere (the company itself did not have office space and everyone was working remotely). She did this for the first 9 months of our first year of nomadic travel because it was worthwhile to maintain her salary while our cost of living dropped to more than half in 2018 as we became nomadic).

During this time, both of us where covered by Mrs. NN’s employer sponsored healthcare plan. This stopped as of April 1st so we had to decide what to do. Since we were going to spend April to early June in California and knew that not having health care coverage in the USA was no joke (*), we decided to purchase health insurance through the Affordable Care Act. Since our income was estimated to be very low in 2019 with the both of us not working, we could get a Bronze plan (with an acceptable $12,600 family deductible to support us in case of catastrophic emergency, while our emergency fund would take care of the high deductible). This plan was worth about $10,000 per year and thanks to the subsidy, we will only pay $1 per person and per month (or $8 for the last few months of our first year of nomadic travel).

“66.5 percent of all bankruptcies were tied to medical issues”

This is the real reason most Americans file for bankruptcy – CNBC Article

“Unless you’re Jeff Bezos, people don’t have very good alternatives, because the insurance that is available and affordable to people, or that most people’s employers provide them, is not adequate protection if you’re sick.”

This is the real reason most Americans file for bankruptcy – CNBC Article

“Despite gains in coverage and access to care from the ACA, our findings suggest that it did not change the proportion of bankruptcies with medical causes.”

Article on study published in the American Journal of Public Health states

Year 2 of Nomadic Travel

Since the ACA only covers us in California and we were traveling around the world, we had to find something else. We basically had two options that we investigated: travel insurance or expat insurance.

Travel insurance covers for you and your travel. Travel insurance includes a bunch of options you can subscribe to. Here are some of the most common ones:

- “Trip cancelation/interruption” – This will usually cover for all expenses you made if your trip had to be cancelled (usually for emergency situations) prior or during the trip.

- “Gear protection” – This will cover your gear in case it got damaged or stolen.

- “Medical evacuation” – This will cover you if your medical condition required to get you transported to the local hospital or back home to receive treatment.

In a nutshell, this insurance makes more sense for “short trips” to give you peace of mind when you travel or if you have great health coverage in your home country.

Expat Medical Insurance provides medical insurance wherever you are in the world. Similar to health insurance in the USA, your premium is usually a function of:

- Coverage level (or metal) – They are usually Bronze, Silver, Gold and Platinum

- Area of coverage – This can be the entire world, or the entire world without the USA

- Deductible

- Maximum Limit

Based on our situation, we decided to purchase a policy with Gold level coverage (the insurance pays 80% and we pay 20%), a Maximum Limit of $5,000,000 and a deductible of $5,000. This means that we will incur the expense ourselves up to our deductible before the insurance kicks in, covering 80% of our expenses, up to our Maximum Limit. This works for us because we feel comfortable paying out of pocket on all health expenses overseas rather than putting money towards the insurance itself.

This insurance covers us for any catastrophic event (let’s say we have to stay hospitalized for many days or go under extensive surgery) where the cost might go way beyond $5,000 and for this it would be important to have an insurance take care of 80% of the bill.

We purchased this insurance into our 2nd year of travel with IMG Global. The cost of our insurance policy for the two of us was $3,130 ($1,906 for Mrs. NN + $1,224 for myself) as of July 2019. The significant difference in price between Mrs. NN and I is due to “gender rating” that state women are considered a higher risk than men because they tend to visit the doctor more frequently, live longer and have babies. (Note: Whether or not women truly cost health indsurance comapnies more money is actually up for debate).

What the heck is this terminology

Reading through the details and brochures on health insurance is no fun and I realized while writing this article that it might be useful to go over some terminology to help you digest all the insurance lingo.

- What is a Metal (or levels of plans)? These are usually defined as Bronze, Silver, Gold or Platinum. They are based on how you and the insurance plan splits costs. The higher the level the more the insurance will cover you (but also the more expensive the premium will be). A Bronze level means that you will be covered at 60% by your insurance and you will have to pay 40% out of pocket (or 60/40). Silver is usually 70/30. Gold is 80/30 and Platinum is usually 90/10.

- What is an Insurance Carrier/Provider? This is the name of the company providing insurance.

- What is an Insurance Policy? This is the specific contract/document that details the terms and conditions of a contract of insurance. This is basically the document that you will go through if you need to dispute a specific claim.

- What is a Claim? This is the request to an insurance company for coverage / compensation for a covered loss of policy event.

- What is a Premium? This is the amount of money you pay for the health insurance. They are usually paid monthly.

- What is a Deductible? A deductible is the amount of money you will have to pay using your own money (or Out Of Pocket) before your insurance can kick in.

- What is an Out Of Pocket cost? This is basically money you need to pay yourself.

- What is a Maximum Limit? This is the limit of medical expenses after which the insurance will stop covering you.

What about the ACA in 2020?

Since California will require that all its resident has healthcare coverage in 2020, we are still looking to apply for the ACA (assuming we still qualify for the premium subsidy) for $24 per year, which is still lower than the penalty we would have to face otherwise for not applying (ie. a penalty of $695 per uninsured adult, or 2.5 percent of household income).

True cost of health care outside of the USA

As a French person who spent 25+ years living in France, I can tell you that the cost of healthcare can be affordable. Here are a few examples (as of 2019) of the out of pocket cost for someone that would be in France. These are costs you would pay if you come visit France(as a foreigner, it’s of course free for French people) and need to see a doctor:

- General Physician: 23 EUR

- Gynecologist: 25 EUR

Amazing right? Another firsthand data point: Mexico. We spent 3.5 months in Mexico and on one of our weekend hikes in San Miguel de Allende, one of the hikes fell on her arm and broke it. It was a Sunday so we had to get her to the nearest Emergency Care which we saw was very modern, English-speaking and well-equipped. As an American, she was rightfully very worried about the healthcare expenses but in the end she had to pay 136 USD for a visit to the emergency room (including an x-ray). The painkiller prescription was 16 USD. A few days later, the doctor had to drive over from a town about an hour away. He took two additional x-rays (for 35 USD) and the patient paid him 40 USD for having him come over. So the total for 1 ER visit + 3 x-rays + 1 prescription + 1 follow up doctor consultation was about 227 USD. The same treatment in the USA would have easily cost thousands of dollars.

[In Mexico,] the total for 1 ER visit + 3 x-rays + 1 prescription + 1 follow up doctor consultation was about 227 USD. The same treatment in the USA would have easily cost thousands of dollars.

We are going to Thailand next week and will be able to get more data to add here as we plan on getting our teeth cleaned in Chiang Mai but will also keep our eyes open on health care cost.

Why long-term travel is the best health insurance plan you can get

As of 2014, the United States healthcare system was the most expensive in the world while consistently showing that the country underperforms related to others countries (source).

The U.S. […] ranks behind most countries on many measures of health outcomes, quality, and efficiency. U.S. physicians face particular difficulties receiving timely information, coordinating care, and dealing with administrative hassles

“How the U.S. Health Care System Compares Internationally” – The Commonwealth Fund

If we had decided to stay in the US for an extended period of time, it was clear that we would need healthcare insurance if we depended on the medical system.

By becoming world travelers, we have greater control over our budget which includes cost of healthcare. A lot of countries provide a similar level of care (if not better) at a fraction of the cost so we feel comfortable using out of pocket dollars rather than spending thousands of dollars on monthly premiums. For peace of mind, we decided to supplement paying for healthcare out of pocket with a private global expat insurance which is a fraction of the cost of a similar policy purchase within the US for the time being.

Our bottom line

If you are a US resident and won’t have an employer sponsored health insurance plan, you should definitely look at the cost of healthcare insurance in the US and compare this to traveling or living outside of the country. As we demonstrated in this blog post, there are several countries in the world that have amazing cost of living and great affordable healthcare that would lower your overall spending and can increase your quality of life.

Ultimately, healthcare is a very personal decision and unfortunately can be very overwhelming and confusing. We did a ton of research, weighed the pros and cons and decided on what would work best for our situation. We hope our experience and research can help you with your decision making process and make you aware of the options out there.

Note: If you are interested to know more about this topic, we recommend reading the Expat Medical Insurance and Medical Tourism blog post from our friends at All Options Considered that provides an excellent take on how to get started with Expat Medical insurance.

What about you? How do you feel about healthcare in the US? Have you estimated your cost of healthcare in the US today vs retirement? If you are not in the US, would you mind sharing how much it costs you to pay for healthcare premiums in your country?

{kind=link}

22 Comments

The Frug · October 7, 2019 at 10:23 pm

Great post. In researching this I also discovered that Cigna has an international option that allows up to 6 months in the US. The plan runs about half of what our current Cigna high deductible plan and has a lower deductible. Worth a look. Search Cigna Global.

Mr. Nomad Numbers · October 8, 2019 at 6:56 am

Thanks The Frug! This sounds interesting. Do you know if they qualify for the ACA marketplace? When I searched the market place in March (in California) the only carriers that were available to us where either Kaiser, BlueShield, CCHP and Health Net. I’ve heard that more carrier might be coming into the CA marketplace next year so I’ll look again.

Retired at 39 · October 8, 2019 at 8:47 am

I like your pie chart of expenses at the top. However, I don’t think the color coding is working right. For example, it looks like you spent $2,533 on snacks based on the orange color but I can see in the table on the left that this was the local transportation cost. Just wanted to let you know so you could take a look at it.

Mr. Nomad Numbers · October 8, 2019 at 3:19 pm

Hi Retired at 39! We have a bit of a sweet tooth but definitely not for the amount $2,533 / year 🙂

For context, this chart is automatically generated from the tool I built over the summer to help us expedite travel expense planning/tracking and it looks like you find a bug in our tool! I just fix it and was able to re-upload a version of this graph to the post. Thanks for calling this out.

Note: If you are on our mailing list, you should have received an early access to our tool since we plan to open it to everyone once it is ready. If you are not on our newsletter, well what are you waiting for? Also please contact us via our contact form as we would be happy to give you an early access!

Skip · October 9, 2019 at 1:54 am

Great post guys. This is an important topic. Healthcare costs are a big motivating factor in our decision to slow travel internationally vs. remaining in the US. It just makes sense to us since we want to travel anyway.

I haven’t taken a look recently, but I do recall some plans that allow you to stay in the U.S. for for a certain amount of time during the year, as pointed out by Frug. Initially, I don’t see us spending more than a month or two in the U.S. per year.

It is interesting that your plan has a maximum that they will pay vs. the out of pocket maximum that I’m used to seeing in my current employer based insurance.

Did you consider any other plans?

Safe travels.

Mr. Nomad Numbers · October 9, 2019 at 10:08 am

Hi Skip. Glad you like our post. It is actually a pretty big topic and with this article we are just scratching the surface actually. We could write more specific article if our community want to know more about it. We are also learning along the way so I am sure that our current solution will evolve over time. As for the other plans, we looked at World Nomads but then realized that they were just a travel insurance, so not a fit for us. We also looked at Allianz Care. “The Frug” also mentioned Cigna that we will be looking into as our renewal come up next year. I hope this helps!

Lee · November 4, 2019 at 12:50 am

I’ve been nomadic for two years. We launched mid-year, so ACÁ was put in place that year, and we moved to WA before launch. That meant we had to change plans, and went with a Silver Kaiser plan with subsidy. The next year, DH qualified for Medicare, and was not accepted for expat coverage, so I got a bare bones travel ins plan for him ($980). For myself, I got an expat plan from GeoBlue. Cost was $733/mo (age 63) which is probably Gold. I can travel in the US, but no more than 21 days. I am shopping now for next year, and am undecided. If I can get catastrophic only coverage, that will be my choice.

Mr. Nomad Numbers · November 9, 2019 at 2:56 am

Thank you Lee & great to hear that you’ve decided to become nomadic! Can you explain why you can only travel in the US for no more than 21 days? Is this related to the travel insurance you contracted?

laurel · October 10, 2019 at 10:37 am

Thank you for the post. Any and all examples of health care costs as you travel are valuable.

I know some nomads choose to self insure because healthcare in other countries is so reasonable, I.e. hip replacement in Ecuador ~10K, baby delivery in Costa Rica 5k.

A bit scary to consider as an American, but on the other hand, I wonder how well global insurance pays/reimburses for catastrophic care. Hopefully you won’t have to use it, but it would be interesting to see how well it works if you hear of examples.

Mr. Nomad Numbers · October 10, 2019 at 4:56 pm

I was holding on writing this blog post until we did actually occurs bills that we needed to get reimbursed by our expat insurance to provide a more rounded experience but as many readers reach out asking what we were doing wrt health care I decided to share that and we will definitely provide an update if we do need to use them for catastrophic care.

Dragon Guy · October 10, 2019 at 11:49 pm

Thanks for discussing this. The subsidies your are getting for the ACA plans are impressive! Given that Mrs NN. still worked for 3 months this year, how were you able to keep your income so low to get such large subsidies?

I am thinking ahead to my retirement and how to keep our income low enough to get decent subsidies. We expect to be under the 400% of FPL to get some subsidies, but we generate a decent amount of dividends from our taxable accounts. So it’s been challenging to project a really, really, low income to get the highest subsidies.

Mr. Nomad Numbers · October 11, 2019 at 11:35 am

We planned a bit for it 🙂 During the 3 months that Mrs NN worked in 2019, she parked all of her income to law out her 401K whuch resulted in her not receiving much W2 income this year. We expect a combined income of 40K for the two of us (mostly dividends + rental income) which is under the 400% of FP as you know. So hopefully no bad surprise when we file our tax earlier next year.

Dragon Guy · October 12, 2019 at 1:42 am

Ok that makes sense. Interestingly, when I run the numbers with $40k in income, our cost (based on where we live) would be about $80 per month. I picked a random location in CA and did see those low single digit prices you quoted. I never realized there could be such a large difference between locations, even after the subsidies.

Mr. Nomad Numbers · October 12, 2019 at 4:19 am

We used CoveredCalifornia.com as the market place to find our carrier. Did you enter $40K as a married couple?

Dragon Guy · October 12, 2019 at 4:15 pm

Yes I did use $40k. It was interesting to see how in California I could get a plan for two of us for less than $10 a month but in the state we live in it was over $80 per month, using the same income.

Mr. Nomad Numbers · October 13, 2019 at 12:05 pm

It might also have to do with the fact that cost of living in California is one of the highest (of not the highest) in the USA so the threshold might be different. I haven’t looked into that especially but I would not be surprised.

Lee · November 4, 2019 at 1:16 am

Catastrophic Care: I can speak to that! When we launched, DH had a known issue, which meant several carriers declined our application. Cigna however, offered coverage at a great price. I figured they would require a physical or review of records, but instead they immediately approved us.

Four months later, DH needs surgery, which was in Bangkok (Bumrungrad is THE BEST) and successful. However, Cigna put us and our docs through the wringer and then refused coverage, saying if they knew, they would not have offered coverage. Humph.

They refunded all our premiums ($8800) which went a long way toward the bills.

Earlier, I was alone in Bogota, Colombia and broke my leg. It was July 4, so communication with my US insurer wasn’t possible. I paid the cost ($22,000) on my credit card (always keep a high balance available for emergencies) and filed a claim when I returned home. This was the one trip I’d skipped buying travel insurance, ‘natch.

Years ago, I needed surgery on my knee in Bangkok, GeoBlue (was Blue Cross/Blue shield) paid everything without hesitation. That led to my going with them for expat coverage this year. Cigna is a PITA for the medical providers, and slow to pay, (and in our case didn’t) I don’t want the stress when I’m sick.

Mr. Nomad Numbers · November 9, 2019 at 3:02 am

Thank you Lee for sharing all of these details about catastrophic coverage. We’ve noticed that a lot of company that provides expat/nomadic coverage do check for pre-existing conditions and will likely refuse coverage for people with them. Coming from a country where health care if free and available for anyone without such discrimination, this makes me upset and the medical system.

It is a great tip to keep a high balance available. Because why we do have coverage, our insurance will mostly likely ask us to pay the bill and then we will have to submit all the paperwork to get our money back. Would the hospital in Columbia be able to accommodate you if you could not pay everything in full to let you pay overtime in chunk?

Franc · November 19, 2019 at 10:52 am

Thanks for the post. $1,700 on airfare for the year for two people? What kind of hack is this? Was this for only one or two tickets? Did you already make a post on this? Thanking you in advance.

Mr. Nomad Numbers · November 20, 2019 at 6:26 am

Hi Franc.

We have a dedicated article about travel rewards that does into how we save between 6-10K in 2018 alone. The post is here: https://www.nomadnumbers.com/travel-rewards-guide/

While our nomadic year are from

July 1st to June 30th this won’t include the first six month of 2019 but that should give you an idea of the type of savings we manage to get thanks to these generous sign-up bonuses. Let us know if you have further questions!

The true cost of healthcare as nomads - Nomad Numbers · November 18, 2020 at 5:06 am

[…] How to get insured when you travel […]

Experiencing Chinese Medicine in Taiwan — Nomad Numbers · April 5, 2022 at 6:37 am

[…] How to get insured when you travel […]